Commentary – First Quarter 2025

March 21, 2025Commentary – First Quarter 2025

March 21, 2025INSIGHTS

Commentary - Second Quarter 2025

Tailwinds and Tradeoffs:

Positioning for What Comes Next

Our Quarterly Recap & Market Outlook provides insight into the forces shaping the market – beyond the headlines and noise. Connect with us at info@eamoncap.com and take control of your financial future.

QUARTERLY RECAP

We maintain a defensive stance, emphasizing high-quality bonds and stocks with strong fundamentals and a value tilt. Slowing macro data and elevated consumer debt reinforce our caution, yet we see emerging tailwinds—from AI-driven productivity to fiscal support via the OBBBA—that may create selective opportunities. While valuations remain stretched, technicals are supportive in the near term. Should markets retrace, we’re prepared to add risk selectively—leaning into areas with earnings momentum and policy-driven support, while staying anchored in quality.

Despite early signs of volatility through April, expectations for a valuation reset in equity markets proved premature. Rather than a sustained correction, investor exuberance returned with force, reigniting the “buy the dip” mentality and driving prices to fresh highs. By June, market sentiment had shifted modestly toward optimism, supported by easing inflation, resilient consumer demand, and reassuring signals from the Federal Reserve ("Fed").

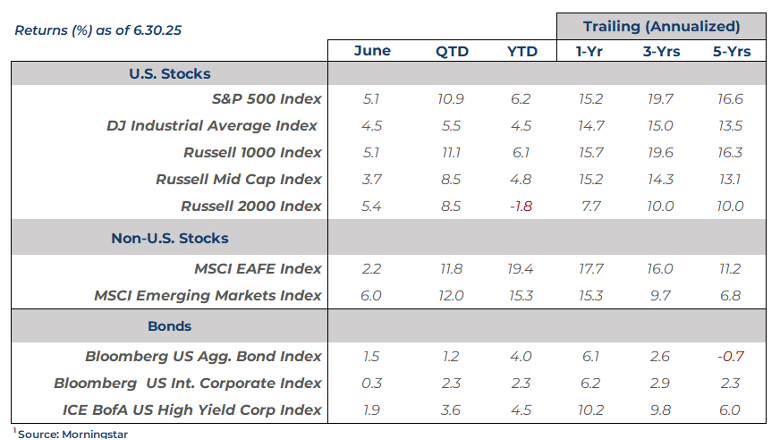

The S&P 500 Index surged +10.9% for the quarter—one of its strongest performances in over two years. The Nasdaq 100 led once again, climbing +18.0%, while the Dow Jones Industrial Average delivered a more measured gain of +5.5%. Bond markets stabilized as rate expectations moderated and credit sentiment improved, with the Bloomberg US Aggregate Bond Index returning +1.2%.

Notably, through the first half of the year, bond returns kept pace with equities: the Bloomberg US Aggregate Bond Index was up +4.0% year-to-date through June 30, compared to just +6.2% for the S&P 500 Index. Until the late-quarter sentiment shift, fixed income had at times outperformed, reflecting cautious positioning and the appeal of yield amid macro uncertainty.

US Economic Growth

Real GDP rose +3.0% in Q2, reversing the statistically distorted -0.5% decline in Q1. The rebound was largely driven by a sharp drop in imports, which had been front-loaded in Q1 ahead of anticipated tariffs. While consumer spending appeared resilient, underlying growth—excluding volatile vehicle purchases—remained soft. Business investment slowed, housing contracted, and inventory drawdowns weighed on output. Despite the headline strength, many economists have noted that the trade and inventory swings may be obscuring a more modest underlying growth trend heading into Q3.

US Inflation

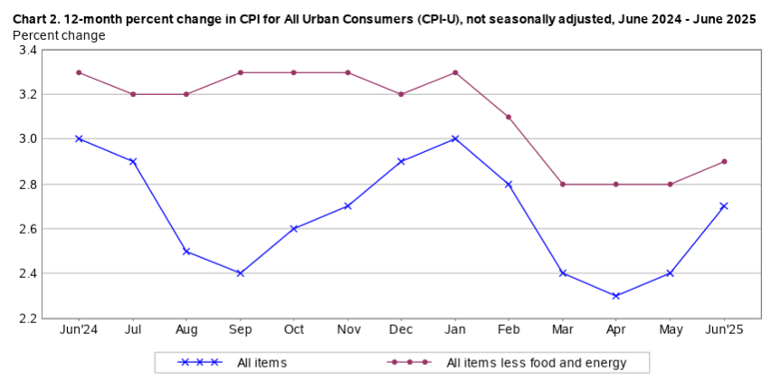

Inflation moderated steadily through the quarter. Headline CPI rose from +2.4% year-over-year in March to +2.7% in June, reflecting a modest but consistent upward trend. Core CPI held firm at +2.9%, underscoring persistent price pressures in shelter, healthcare, and services. Energy inflation eased, with gasoline prices down 8.3% year-over-year, while goods inflation remained subdued amid stable commodity pricing and softening demand. Despite the deceleration, inflation remains above the Fed’s 2% target, and officials remain cautious about entrenched price dynamics.

US Labor Market

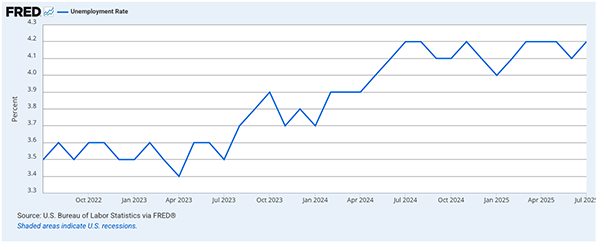

The U.S. labor market is showing clearer signs of deterioration as momentum fades across key indicators. In July, nonfarm payrolls rose by just 73,000—well below consensus expectations—while the unemployment rate edged up to 4.2%. Revisions to May and June payrolls erased a combined 258,000 jobs, casting doubt on earlier signs of resilience. Private-sector hiring contracted for a second consecutive month, and federal employment continued to decline amid budget constraints and a hiring freeze.

June data had already hinted at softening conditions: job openings fell to 7.44 million, the lowest since September 2024, and wage growth remained subdued at 0.2% month-over-month and 3.7% year-over-year. Sectors like health care and state government provided modest support, but transportation and social assistance gains were offset by cuts in professional services and manufacturing.

Taken together, the latest reports suggest that labor demand is weakening more rapidly than previously thought. Businesses appear increasingly cautious in the face of slower consumer spending, tighter credit conditions, and geopolitical uncertainty. While the labor market remains historically tight, the trend is clearly shifting toward slack—raising the stakes for policymakers and investors heading into the fall.

Financial Markets Performance Recap

Stocks

U.S. stocks posted strong gains in the second quarter, led by large-cap and growth-oriented stocks. The S&P 500 Index rose +10.9%, and the Russell 1000 Index advanced +11.1%, reflecting broad-based strength across sectors. The Nasdaq 100 Index surged +18.0%, driven by continued momentum in mega-cap technology. Mid-cap and small-cap stocks also delivered solid returns, with the Russell Mid Cap Index up and Russell 2000 Index both rising +8.5%.

However, year-to-date through June 30, mid-cap stocks posted solid mid-single-digit gains, with the Russell Mid Cap Index up +4.8%. In contrast, smaller, more rate-sensitive companies continued to face headwinds, as reflected in the Russell 2000 Index’s -1.8% decline over the same period.

For the quarter, growth significantly outperformed value across all market capitalizations. In large caps, the Russell 1000 Growth Index gained +17.8%, far outpacing the Russell 1000 Value Index at +3.8%. Among mid caps, the Russell Mid Cap Growth Index returned +18.2%, while the Russell Mid Cap Value Index lagged at +5.3%. In small caps, the Russell 2000 Growth Index rose +12.0%, ahead of the Russell 2000 Value Index at +5.0%.

International equities also posted strong quarterly gains. The MSCI EAFE Index rose +11.8%, with growth outperforming value—MSCI EAFE Growth Index up +13.5% versus MSCI EAFE Value Index at +10.1%. The MSCI Emerging Markets Index advanced +12.0%, supported by improving sentiment across Asia and Latin America. International small caps showed notable strength, with the MSCI ACWI ex U.S. Small Cap Index up +16.9%.

Bonds

Fixed income markets posted modest gains, as investors adjusted expectations around the Fed's policy and inflation remained contained. The Bloomberg U.S. Aggregate Bond Index rose +1.2%, with intermediate-term bonds slightly outperforming at +1.5%. Short-term government and credit bonds gained +1.3%, offering stability amid modest rate volatility.

High-yield corporate bonds led with the ICE BofA U.S. High Yield Index up +3.6%, supported by strong investor demand and resilient credit conditions. Inflation-protected securities were more subdued, with the Bloomberg U.S. Treasury Inflation-Protected Securities (TIPS) Index rising just +0.5%.

Long-duration corporate bonds posted muted returns, with the Bloomberg U.S. Long Corporate Index up +1.2%, reflecting sensitivity to rate movements and modest spread widening.

Emerging market debt was a standout. The J.P. Morgan GBI-EM Global Diversified Index surged +7.6%, driven by local currency strength and improving sentiment across select economies. A weakening U.S. dollar further boosted returns, since investors holding bonds denominated in local currencies saw those currencies rise in value relative to the dollar. Hard currency sovereign debt (bonds denominated in U.S. dollars) also advanced, with the J.P. Morgan EMBI Global Diversified Index up +3.3%, supported by renewed demand for yield and stabilizing credit conditions.

Want to uncover the complete picture of how the market might unfold? Our exclusive newsletter delves into more than just current trends.

You'll discover:

Our in-depth market outlook: Uncover the forces shaping the coming months and their potential impact on your portfolio.

Expert portfolio positioning: See how we strategically adjust portfolios to capture opportunities amidst shifting market conditions.

Actionable insights: Gain tailored guidance to navigate challenges and capitalize on potential upsides.

Simply connect with us at info@eamoncap.com and take control of your financial future.

Eamon Capital Management, LLC (“Eamon”) is a registered investment advisor offering advisory services in the State of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Eamon Capital Management, LLC (referred to as “Eamon”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute Eamon’s judgement as of the date of this communication and are subject to change without notice. Eamon does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Eamon be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if Eamon or a Eamon authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.