Market Update: August 2025

August 16, 2025Market Update: August 2025

August 16, 2025INSIGHTS

Commentary - Third Quarter 2025

Market Overview

The fourth quarter of 2025 closed out a volatile but ultimately constructive year for global financial markets. Sentiment improved modestly in December as inflation stabilized, economic data remained mixed but resilient, and investors grew more confident that the Federal Reserve was nearing the end of its tightening cycle.

Our Quarterly Recap & Market Outlook provides insight into the forces shaping the market – beyond the headlines and noise. Connect with us at info@eamoncap.com and take control of your financial future.

QUARTERLY RECAP

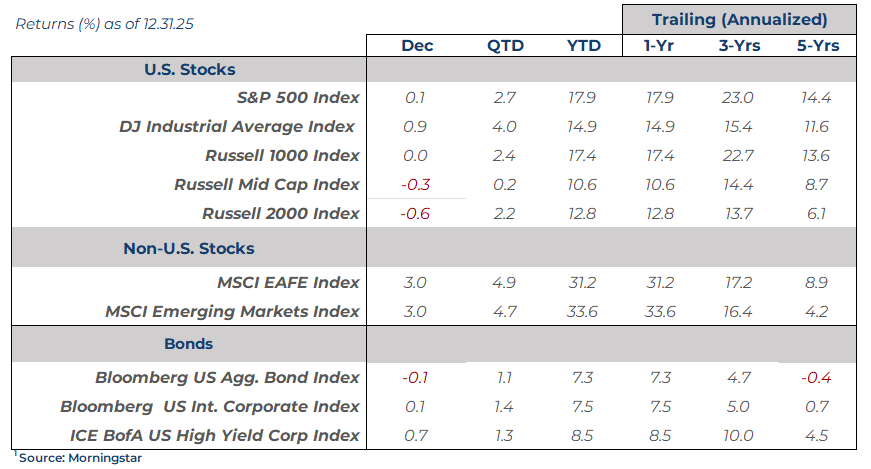

The S&P 500 gained +2.7% for the quarter, bringing its strong full‑year performance to +17.9%. The Nasdaq 100 once again outpaced broader indices, rising +2.5% in Q4 and +21.0% for the year, while the Dow Jones Industrial Average delivered a more measured +4.0% gain in Q4 and +14.9% for 2025. Bond markets also advanced as shorter yields drifted lower, with the Bloomberg U.S. Aggregate Bond Index returning +1.1% in Q4 and +7.3% for the full year amid improving rate expectations and steady credit conditions.

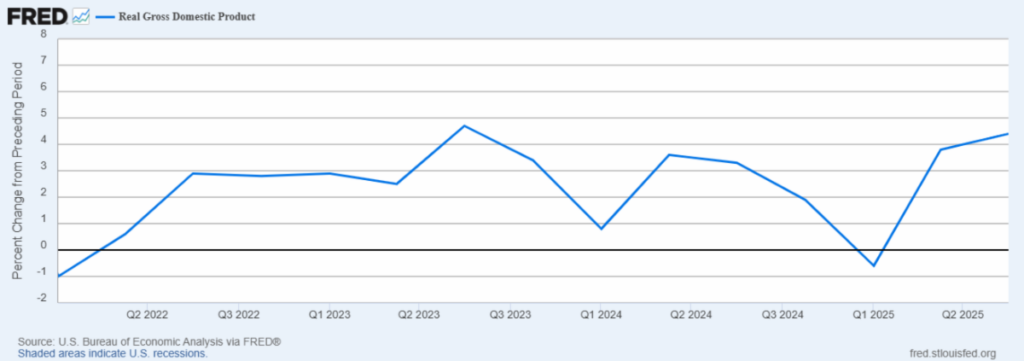

US Economic Growth

|

Real GDP for Q4 has not yet been released, but early estimates point to a slower pace of expansion following the strong, trade‑boosted Q3 forecast of roughly+4.0%. Consumer spending remained the primary engine of growth, though the composition continued to shift toward services as durable goods demand softened. Business investment was mixed—intellectual property spending held firm, but equipment and structures remained sluggish, reflecting tighter financial conditions and more cautious corporate sentiment. Trade flows normalized further after the Q3 import rebound, removing a temporary tailwind, while inventory restocking was modest and unlikely to provide meaningful support to output. Taken together, the data suggest that while headline growth may remain positive, underlying momentum is cooling as the economy transitions into 2026. |

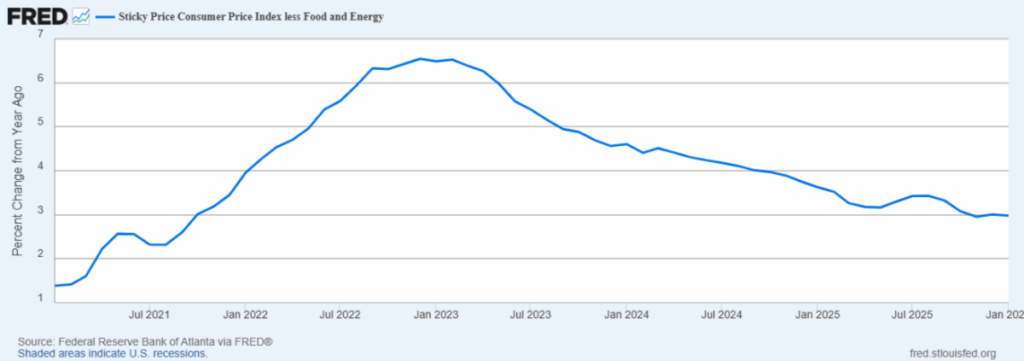

US Inflation

|

Inflation showed signs of stabilizing in Q4 but remained above the Federal Reserve’s +2.0% target. Headline CPI held near +3.0% year‑over‑year, while core CPI—excluding food and energy—also hovered around +2.6%, underscoring persistent price pressures in shelter, healthcare, and other service‑sector categories. Energy prices were more stable compared with earlier in the year, though utility costs remained elevated. Core goods inflation stayed firm due to ongoing tariff pass‑through effects in categories such as apparel and household furnishings. Market‑based inflation expectations, including the 5‑year forward breakeven rate near +2.3%, continue to suggest that investors expect inflation to gradually converge toward the Fed’s target. Still, with both headline and core inflation running above 2%, policymakers maintained a cautious stance heading into 2026. |

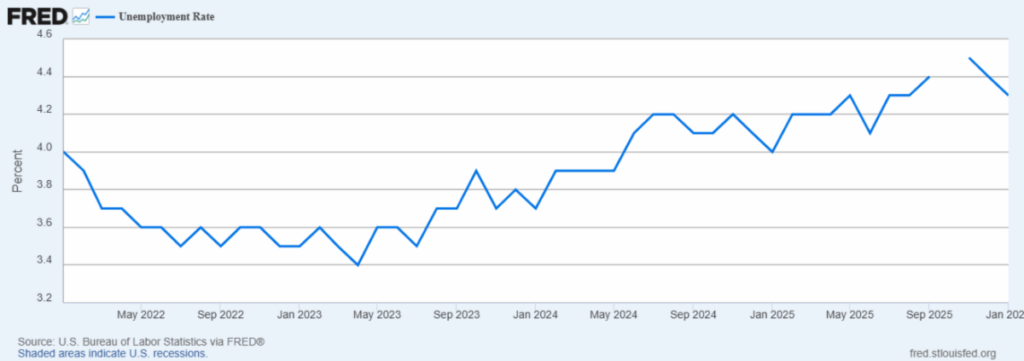

US Labor Market

Labor market conditions softened further in Q4 as hiring momentum continued to fade from its mid‑year peaks, and the most recent data reinforced that cooling trend. Monthly payroll gains through the final quarter averaged roughly 115,000, and January’s report showed employers added 130,000 jobs, a still‑moderate pace that aligns with the broader slowdown seen over the past year. The unemployment rate ended the year at 4.3%, holding near its highest level in more than two years and reflecting a gradual rebalancing of labor supply and demand.

Revisions to prior months’ data continued to point toward weaker underlying job creation, with December revised down to 48,000 and annual benchmark adjustments reducing previously reported payrolls by nearly 900,000. Job openings fell to 6.5 million, the lowest level in more than five years outside the pandemic period, signaling a clear downshift in labor demand. Wage growth eased to 3.7% year‑over‑year, with average hourly earnings rising 0.4%month‑over‑month—enough to help cool inflation pressures but also consistent with softer hiring appetite.

Gains remained heavily concentrated in healthcare, social assistance, and construction, while several private‑sector industries saw little to no net hiring. Overall, while the labor market remains resilient by historical standards, the trend clearly shifted toward slack in late 2025, raising the stakes for the Federal Reserve as it weighs the risks of maintaining restrictive rates against emerging signs of a cooling economy.

Financial Markets Performance Recap

U.S. Stocks

Equity markets ended 2025 on firmer footing, though leadership narrowed and volatility picked up as investors reassessed earnings strength and the path of interest rates. U.S. Large‑cap stocks continued to anchor performance, with the S&P 500 up +17.9% for the year (+2.7% in Q4). The Russell 1000 delivered a similar +17.4% (+2.4% in Q4), while the tech-heavy Nasdaq 100 led major benchmarks at +21.0% (+2.5% in Q4).

Growth stocks maintained a full‑year advantage, but value outperformed late in the year as investors rotated toward steadier cash‑flow businesses. The Russell 1000 Growth returned +18.6% (+1.1% in Q4), while the Russell 1000 Value gained +15.9% (+3.8% in Q4).

Mid‑cap and small‑cap stocks delivered more mixed results. The Russell Mid Cap Index rose +10.6% (+0.2% in Q4), with mid‑cap growth lagging at +8.7% (‑3.7% in Q4). Mid‑cap value held up better at +11.1% (+1.4% in Q4). Small caps showed a similar pattern: the Russell 2000 gained +12.8% (+2.2% in Q4), with value at +12.6% (+3.3% in Q4) and growth at +13.0% (+1.2% in Q4).

Non-U.S. Stocks

International equities delivered some of the strongest returns of the year. Developed markets surged, with the MSCI EAFE Index up +31.2% (+4.9% in Q4). Value led by a wide margin: EAFE Value +42.3% (+7.8% in Q4) versus EAFE Growth +20.8% (+1.9% in Q4). Emerging markets also posted strong results, with the MSCI EM Index up +33.6% (+4.7% in Q4). International small caps were another standout at +29.3% (+3.0% in Q4).

Across global markets, the fourth quarter reflected a subtle but important shift: while mega‑cap growth continued to dominate full‑year results, Q4 saw a rotation toward value, cyclicals, and international markets. This broadening of leadership suggests investors are beginning to look beyond the narrow set of companies that drove much of 2025’s gains, positioning markets for a more balanced environment heading into 2026.

Bonds

Bond markets delivered solid results in 2025 as inflation eased and major central banks began lowering interest rates. The Bloomberg U.S. Aggregate Bond Index returned +7.3% for the year (+1.1% in Q4), supported by falling short‑term yields and steady credit conditions. Shorter‑maturity bonds also performed well, with the Bloomberg U.S. Gov’t/Credit 1–3 Year Index up +5.4% (+1.2% in Q4), reflecting the early stages of the Fed’s easing cycle.

High‑yield bonds benefited from improving risk sentiment, with the ICE BofA U.S. High Yield Index gaining +8.5% (+1.3% in Q4). Inflation‑protected securities also advanced as real yields moderated, with the Bloomberg U.S. TIPS Index up +7.0% (+0.1% in Q4). Longer‑duration corporate bonds saw some of the strongest gains as interest‑rate volatility declined, with the Bloomberg U.S. Long Corporate Index rising +7.4% (-0.1% in Q4).

International bonds contributed meaningfully as well. Emerging‑markets local‑currency debt continued to benefit from high real yields and stronger currencies, with the J.P. Morgan GBI‑EM Global Diversified Index up +19.3% (+3.3% in Q4). Hard‑currency, or U.S. dollar-denominated, EM debt also performed well, with the J.P. Morgan EMBI Global Diversified Index returning +14.3% (+3.3% in Q4).

Across fixed‑income markets, the combination of easing inflation, improving growth, and coordinated rate cuts created a more supportive backdrop for bond investors heading into 2026.

Want to uncover the complete picture of how the market might unfold? Our exclusive newsletter delves into more than just current trends.

You'll discover:

Our in-depth market outlook: Uncover the forces shaping the coming months and their potential impact on your portfolio.

Expert portfolio positioning: See how we strategically adjust portfolios to capture opportunities amidst shifting market conditions.

Actionable insights: Gain tailored guidance to navigate challenges and capitalize on potential upsides.

Simply connect with us at info@eamoncap.com and take control of your financial future.

Eamon Capital Management, LLC (“Eamon”) is a registered investment advisor offering advisory services in the State of Pennsylvania and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Eamon Capital Management, LLC (referred to as “Eamon”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute Eamon’s judgement as of the date of this communication and are subject to change without notice. Eamon does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall Eamon be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if Eamon or a Eamon authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.